Workers’ compensation for a staffing company operates differently from workers’ comp for a regular business. The risk profile is broader, the underwriting process is more involved, the program options are more varied, and the financial stakes are higher. Staffing owners who treat workers’ comp as a standard business insurance purchase typically overpay, choose the wrong program, or both.

This post covers the four core differences every staffing firm owner needs to understand before buying or renewing a workers’ comp policy.

1. Your Employees Work in Dozens of Different Environments

A regular business has one location. The carrier knows the building, the machinery, the job types, and the safety environment. The risk is contained and relatively straightforward to evaluate.

A staffing company sends its employees to dozens or hundreds of different client locations. Each location has different machinery, different tools, different personnel, and different safety protocols. A warehouse staffing firm might be placing workers at 50 different distribution facilities. Each one has its own forklift procedures, loading dock standards, and injury history. The carrier is evaluating all of those environments, not just the staffing company’s own office.

This is why staffing company owners and managers need to actively evaluate each client location before placing workers there. Understanding a client’s safety practices, equipment, and workplace culture is not optional. It directly affects the staffing company’s claims history, and claims history directly affects workers’ comp rates at renewal.

Safe client environments benefit the staffing company financially, not just the workers physically. This is especially true for light and heavy industrial placements, where workers’ comp rates are among the highest of any industry vertical.

2. The Underwriting Process Is More Involved

Underwriting for a regular business workers’ comp policy can often be completed online in minutes. The application is straightforward, the risk is contained, and most carriers return a quote quickly.

Underwriting for a staffing company workers’ comp policy takes longer and requires more information. For light and heavy industrial staffing, carriers want historical claims data from the staffing company and from the staffing company’s clients. They are building a picture of actual workplace injury experience across the entire operation, not just the staffing firm’s own reported history.

This process can take several days. Staffing owners should plan for it and work with a broker who knows how to prepare and present the underwriting package accurately and favorably.

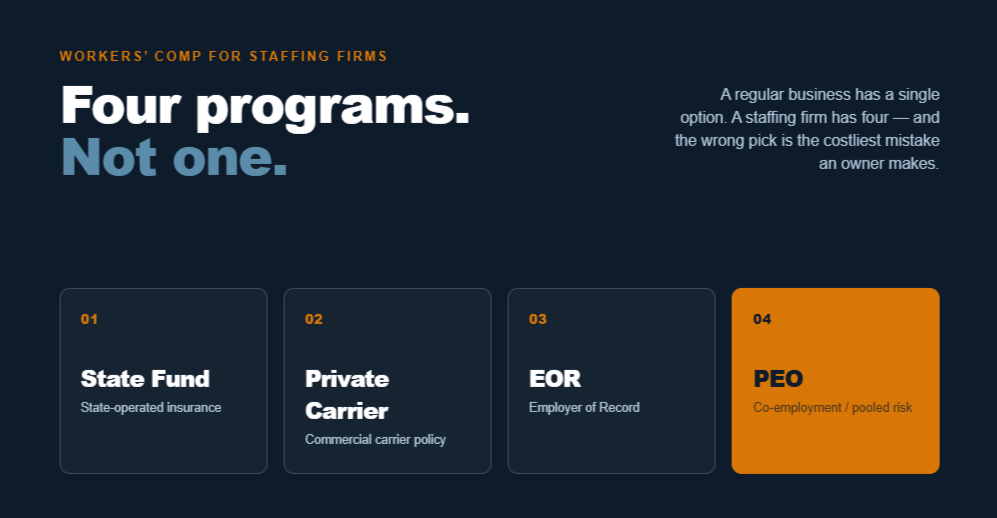

3. There Are Four Program Options, Not One

Most regular businesses have one realistic workers’ comp option: a private carrier policy. Staffing companies have four distinct program types, each with different cost structures, cash flow implications, eligibility requirements, and operational considerations.

The single most expensive mistake a staffing firm owner makes is not evaluating all four options before purchasing. It takes a broker with genuine staffing industry experience to understand, analyze, and explain each program type in the context of a specific staffing firm’s situation.

State fund workers’ comp. Coverage through the state-operated insurance fund. Available in all states and mandatory in some. Sometimes the most competitive option for newer staffing firms with limited claims history.

Private carrier workers’ comp. Coverage through a commercial insurance carrier. The most common arrangement for established staffing firms. Rates and terms vary significantly by carrier and by the staffing verticals a firm operates in.

Employer of Record (EOR) workers’ comp. Coverage provided through an EOR arrangement, where a third-party employer of record takes on the employment relationship and the associated workers’ comp exposure. Can be cost-effective for specific staffing scenarios.

Professional Employer Organization (PEO) workers’ comp. Coverage through a PEO, which co-employs the staffing company’s workers. PEOs pool risk across their client base, which can produce favorable rates for staffing firms that might otherwise be difficult to insure individually.

Each program has a different cost structure, a different cash flow impact, different eligibility requirements, and different implications for how the staffing business operates. A staffing workers’ comp specialist is the professional equipped to evaluate all four options for a specific firm’s situation and recommend the right fit.

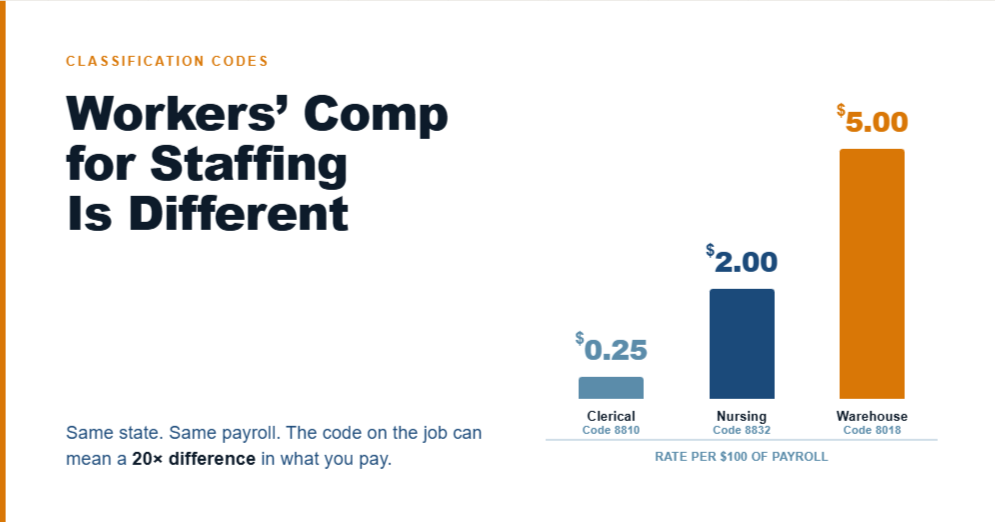

4. Classification Codes Determine What You Pay

There are approximately 700 active workers’ comp classification codes used nationwide to categorize workplace risk and calculate premiums. For staffing companies, getting these codes right is a financial decision with direct bottom-line consequences.

The specific codes that apply to a staffing business depend on the industry verticals the firm works in and the codes already assigned to the firm’s clients, referred to as the governing code. A few examples illustrate how significant the rate differences can be:

Code 8832 (Nursing, healthcare vertical): Rated approximately $2.00 per $100 of payroll.

Code 8018 (Light industrial warehouse): Rated between $3.00 and $7.00 per $100 of payroll.

Code 8810 (Clerical and office workers): Rated approximately $0.25 per $100 of payroll.

Code 8742 (Outside sales): Applies to sales positions even in otherwise white-collar industries.

Code 8748 (Auto firm salesperson): A specific code for a specific role even within the same general business category.

The difference between the clerical code rate and the warehouse code rate is not a small variance. It reflects that a warehouse worker is doing a materially higher-risk job than an office worker, and the premium structure reflects that actuarial reality. The rate for a warehouse worker in a specific state may be $5.00 per $100 of payroll. The rate for a clerical worker in the same state may be $0.25 per $100 of payroll.

Carriers audit all staffing companies at least once a year. They are verifying that the correct codes are being assigned to each job and each employee. A misclassification can result in a large audit bill when the carrier adjusts the premium to reflect the correct code and rate for the actual work being performed.

The exact, detailed job description for each position matters. ‘Warehouse worker’ is not specific enough. ‘Forklift operator in a refrigerated distribution facility’ is specific enough. The more precisely a job is described, the more accurately it can be coded, and the less exposure the staffing company has to an audit surprise at year end.

Why Cash Flow Matters as Much as Rate

Staffing companies operate on thin margins. This is one of the defining financial realities of the industry, and it makes workers’ comp purchasing decisions more complex than they are for most businesses.

Two staffing companies can be quoted the same base rate and end up with very different effective costs depending on the structure of the program they choose. Workers’ comp deductibles, deposit requirements, premium payment schedules, and whether premiums are fixed or variable all affect the actual cash flow impact of a policy.

For new and small staffing companies with limited reserves or retained earnings, a program that requires a large upfront deposit can create an immediate cash flow problem even if the annual rate looks competitive. Pay-as-you-go programs tie premium payments directly to payroll as it is processed, eliminating the deposit requirement and smoothing out cash outflow over time. For a growing staffing firm with fluctuating headcount, this structure can be worth more than a rate reduction.

What This Means for How You Buy Workers’ Comp

Workers’ comp is not a commodity purchase for a staffing firm. It is one of the most consequential financial decisions a staffing owner makes, and it requires a broker who understands the staffing industry specifically.

The right broker evaluates all four program types for the firm’s specific situation. They understand governing codes and how client classifications affect rates. They factor in cash flow when recommending a program structure, not just the headline rate. They stay involved through the audit process to make sure the year-end reconciliation does not produce unexpected charges.

Staffing firms that are renewing with the same carrier and program year after year without shopping all four options are frequently leaving money on the table.

Frequently Asked Questions

Why can’t I just buy workers’ comp online like other business insurance?

For simple, single-location businesses in low-risk industries, online workers’ comp purchasing works fine. For staffing companies placing workers in light or heavy industrial roles, the underwriting process requires more information and more time because the carrier is evaluating risk across all client locations. A broker who specializes in staffing workers’ comp manages this process and presents the underwriting package in the way most favorable to the firm.

How often should a staffing firm review its workers’ comp program?

At minimum once a year, at renewal. Any time the business materially changes, including adding a new industry vertical, a major new client, or significant payroll growth, is also a good trigger for a review. Rate environments change, new program options emerge, and claims history evolves. A program that was the right fit two years ago may not be the most cost-effective option today.

What happens if I assign the wrong classification code to a worker?

The carrier will catch it at the annual audit. If workers were assigned a lower-rate code than their actual job warranted, the carrier will calculate the additional premium owed for the difference and invoice the staffing company. Depending on the volume of misclassified workers and the rate differential, this can be a substantial unexpected charge. Working with a broker who understands coding from the start eliminates most of this exposure.

Does my clients’ safety record affect my workers’ comp rates?

Yes, directly. Workers’ comp claims experience is based on injuries that happen to the staffing company’s employees, which happen at client locations. A client with poor safety practices generates more claims, which flows into the staffing company’s experience modification rate (EMR). The EMR affects base rates at every renewal. Evaluating client workplace safety is a financial responsibility, not just a moral one.

What is the difference between a staffing workers’ comp specialist and a general insurance broker?

A general broker may have limited familiarity with the staffing industry’s specific programs, codes, underwriting requirements, and cash flow considerations. A staffing workers’ comp specialist works primarily in the staffing vertical, maintains relationships with carriers that specialize in staffing accounts, understands all four program types and when each is appropriate, and has experience navigating the audit process specific to staffing companies. The difference in outcomes, including rate, program fit, and audit exposure, is typically significant.